Hello, this is MUST Asset Management.

As a shareholder holding approximately 10.21% of Refine Co., Ltd. (the “Company”), we have been actively engaging in various efforts to address concerns regarding shareholder value erosion and governance issues arising from the Exchangeable Bonds (“EB”) resolved for issuance on April 9 of last year, particularly in relation to the new controlling shareholder and management. As part of these ongoing efforts, we would like to publicly express our views and raise questions regarding the agenda for the upcoming general shareholders’ meeting scheduled for March 31, as well as the Company’s FY2025 financial statements disclosed a few days ago.

[Cash Dividend]

First, we would like to thank the management and employees for delivering approximately KRW 18.9 billion in operating profit in FY2025. While this represents a slight decrease from approximately KRW 20.5 billion in FY2024, it nonetheless demonstrates the Company’s stable business model and profitability. We also appreciate management’s decision to declare a cash dividend of approximately KRW 4.5 billion.

Given the Company’s financial position, with approximately KRW 200 billion in excess cash and earnings continuing to accumulate in cash form, we believe that a higher level of cash return (or alternatively, share buybacks and cancellations) could have been a more optimal decision from both a shareholder value and ROE-focused management perspective. That said, considering that the Company had not paid any dividends since its IPO in 2021, we support and welcome this first dividend decision as shareholders.

[Necessity of Capital Reserve Reduction]

However, we have one question.

In the third quarter of last year, we submitted a proposal at an extraordinary general meeting to reduce the capital reserve. However, the proposal was rejected due to opposition from the Company’s controlling shareholder, Realtyfine (holding 8.31 million shares). Among other shareholders, only approximately 60,000 shares voted against the proposal. In substance, the proposal was rejected solely due to the opposition of the controlling shareholder.

Had the proposal been approved, the KRW 4.5 billion dividend to be received this year would have been treated as a tax-free dividend. Instead, it has become a taxable dividend, resulting in most individual shareholders bearing tax burdens of up to approximately 50%. This tax burden will continue to apply to future dividends as well.

Question 1) We would like to ask again the reason behind last year’s opposition decision.

Question 2) If it is difficult to respond to Question 1, we request that the Company promptly re-submit the proposal to reduce the capital reserve at the earliest possible opportunity and vote in favor of it. If any practical assistance is required, we are willing to actively support this as a ~10% shareholder.

[Cause of Net Income Decline: Accounting Treatment of Exchangeable Bonds]

While the Company’s operating profit remained largely stable year-over-year, net income declined by more than half compared to FY2024 (from KRW 20.6 billion to KRW 9.1 billion). This was primarily due to approximately KRW 8.9 billion in financial liability losses recognized as financial expenses in the income statement. Although this is a non-cash accounting expense, we would like to raise serious questions regarding the EB-related accounting treatment based on this.

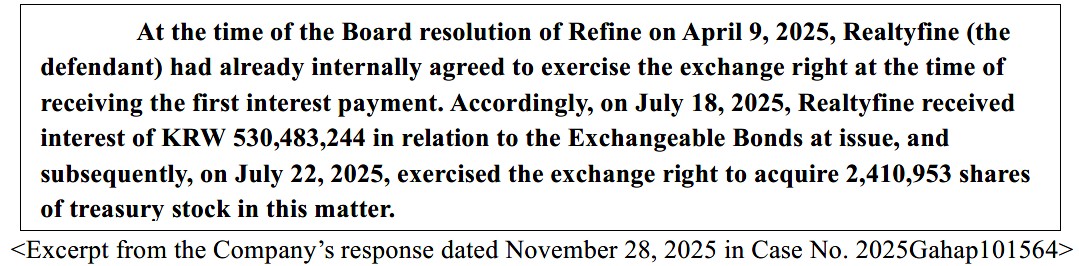

The disclosures in the Company’s semi-annual report (June 2025), quarterly report (September 2025), and annual report (December 2025) do not provide sufficient detail to clearly understand the accounting principles applied. However, when the early exercise of the EB was announced on July 22 last year, both the Company and its controlling shareholder Realtyfine (the EB holder) stated through the media that the decision was made “due to concerns over derivative valuation losses arising from share price increases.”

If this statement is accurate, the approximately KRW 8.9 billion financial liability loss recognized in the FY2025 financial statements appears to reflect derivative valuation losses resulting from share price increases following the issuance of the EB.

However, we question whether this accounting treatment is appropriate.

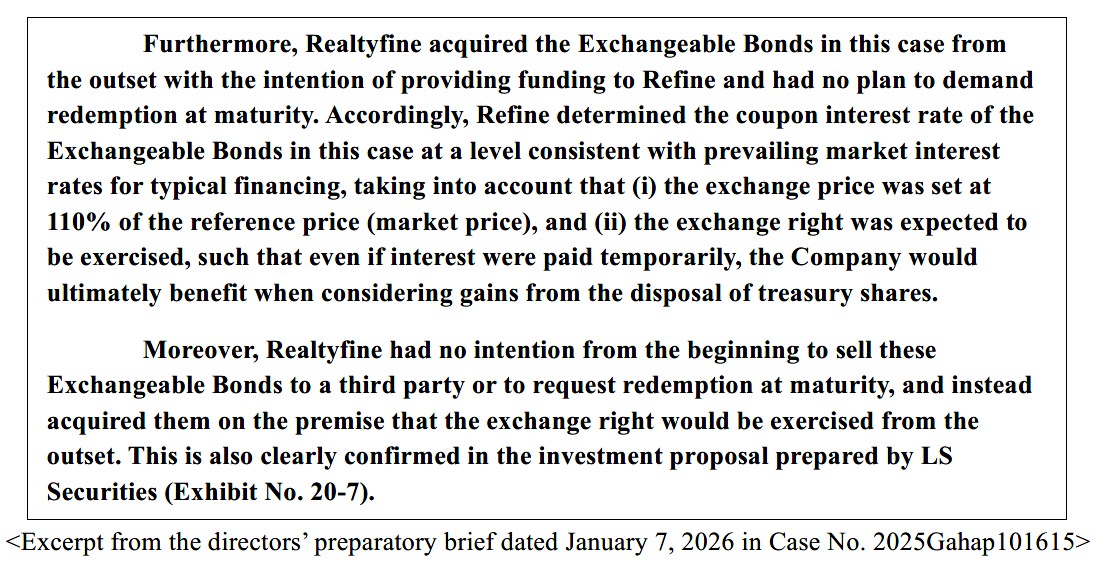

We are currently pursuing litigation to restore to the Company the treasury shares that were disposed of to the controlling shareholder (lawsuit seeking nullification of the EB issuance), as well as a shareholder derivative lawsuit seeking to hold the directors liable for damages caused by the EB issuance. In these proceedings, the Company and its directors have stated that, at the time of the EB issuance, it was already predetermined that the controlling shareholder would receive only one interest payment and then exercise the exchange right early, and that they were fully aware of this fact.

We were deeply confused upon reviewing these court submissions.

First, the explanation provided is entirely inconsistent with the rationale for early exercise previously disclosed to the media.

Second, we made our shareholding disclosure on July 18 and communicated with the Company through private letters up to July 21, and submitted a shareholder proposal for an extraordinary general meeting on July 21. Coincidentally, the decision to exercise the EB was made on July 22.

However, assuming that the statements submitted to the court, arguably the most formal and consequential representations, are accurate, we would like to raise the following accounting-related questions.

Based on consultations with the audit and technical review divisions of major domestic accounting firms, we have been advised that if the issuance terms and early exercise of the exchange right were effectively predetermined at the time of issuance, derivative valuation losses arising from market price changes should not be recognized in the income statement.

Based on this, we raise the following public questions:

Question 1) Was the early exercise of the EB approximately three months after issuance driven by

a) concerns over derivative valuation losses, or

b) a pre-arranged plan at the time of issuance to exercise the exchange right in July?

Question 2) If b) is correct, we request an explanation of the basis for recognizing approximately KRW 8.9 billion in financial liability losses in the FY2025 income statement, as well as the justification for the appropriateness of such accounting treatment.

Was the early exercise plan omitted from disclosure at the time of issuance and not communicated to the auditing firm, resulting in incorrect accounting treatment?

Or, while omitted from public disclosure, was it in fact communicated to the auditing firm, but the auditing firm failed to properly reflect it?

Or, in the most serious scenario, were the submissions made to the court not truthful?

[Director Reappointment Agenda]

We strongly oppose the reappointment of the following five directors—Hyun Seung-yoon, Cho Ju-young, Sung Ik-hwan, Park Su-jin, and Yoon Seung-hyun—who approved the EB issuance that resulted in losses to Refine and gains to Realtyfine, thereby causing significant harm to shareholders of the listed company. Given this history, we do not believe these candidates can be expected to act in the best interests of Refine in situations where conflicts arise between Refine and Realtyfine.

Finally, as mentioned earlier, we would like to inform all shareholders that, as a ~10% shareholder, we are continuing to exercise our shareholder rights as follows to restore value for the Company and all shareholders:

- Seoul Eastern District Court Case No. 2025Gahap101564 (Invalidation of EB Issuance, etc.)

This lawsuit seeks to restore approximately 13.9% treasury shares disposed of to the controlling shareholder back to the Company. Following the filing of the complaint, the Company has submitted its response, and we have submitted a rebuttal brief. We have requested the court to designate a hearing date as of February 19, 2026.

- Seoul Eastern District Court Case No. 2025Gahap101615 (Shareholder Derivative Action)

This lawsuit seeks damages from the directors for losses incurred by the Company due to the EB issuance. After the filing of the complaint, the defendant directors have submitted their responses and preparatory briefs, and a hearing date has not yet been scheduled.

Litigation of this nature, requiring substantial time, cost, and effort, is not easy in the Korean capital markets, and meaningful precedents remain limited. Nevertheless, as an investment firm that has benefited significantly from the capital markets, we are committed to pursuing these actions to achieve meaningful outcomes. We will also ensure that the benefits of such outcomes accrue to all shareholders.

We sincerely ask for your support.

Thank you.

MUST Asset Management